Sunday, June 23, 2024

Monday, June 17, 2024

Freddie Is at It Again

As Yogi Berra would say, “It’s Déjà vu all over again.” Apparently, Government Supported Enterprises (GSEs), Freddie Mac and Fannie Mae, learned nothing from their mortgage backed loan failures and fiascos in 2008-11 which inflicted U.S. taxpayers with total combined losses of $266 and required a $187.5 billion bailout from the U.S. Treasury.

Now according to the Wallstreet Journal Editorial Board, Freddie Mac wants to guarantee second mortgages on homes on which owners have ultra-low first mortgage interest rates, lots of home equity and wish to tap into this equity to pay off current high interest auto and credit card balances. That is, in addition to $7.5 trillion of taxpayer backing at risk, the GSEs wants to get back into taxpayers wallets.

A reduction in equity would once again subject the taxpayer to massive losses from a downturn in home prices and climbing interest rates. The chart below from the Federal Reserve of New York point to the financial risks to the taxpayer.

The GSEs can implement the plan within 60 days unless the FHFA (Federal Housing Finance Authority) vetoes it. There is the temptation to see politics behind this move since it would significantly boost consumer spending as the second mortgage refinancing finds its way onto the street. Not bad for incumbent politicians running for office this November. Ernie Goss

Now according to the Wallstreet Journal Editorial Board, Freddie Mac wants to guarantee second mortgages on homes on which owners have ultra-low first mortgage interest rates, lots of home equity and wish to tap into this equity to pay off current high interest auto and credit card balances. That is, in addition to $7.5 trillion of taxpayer backing at risk, the GSEs wants to get back into taxpayers wallets.

A reduction in equity would once again subject the taxpayer to massive losses from a downturn in home prices and climbing interest rates. The chart below from the Federal Reserve of New York point to the financial risks to the taxpayer.

The GSEs can implement the plan within 60 days unless the FHFA (Federal Housing Finance Authority) vetoes it. There is the temptation to see politics behind this move since it would significantly boost consumer spending as the second mortgage refinancing finds its way onto the street. Not bad for incumbent politicians running for office this November. Ernie Goss

Sunday, February 12, 2023

A Less Painful Spending Cut: Raising Social Security Retirement Age

The U.S. federal government recently hit its debt ceiling of $31.4 trillion, and barring an agreement between the Republican Congress and the Biden Administration, the nation will default on its debt in the first week of June. Republicans are demanding spending cuts, while the Biden Administration declares no to spending outlays. Are there areas of potential agreement? One of the most logical programs to slice is the largest—Social Security (SS) outlays. Even with no reductions to the program, the Congressional Budget Office (CBO) has forecast that the SS Trust fund will be exhausted by 2033, and would demand a 23% reduction in benefit payments to all recipients in 2034.

|

Instead of reducing monthly benefit payments, the retirement age could be changed with legislative action. The original Social Security Act of 1935 set the minimum age for receiving full retirement benefits at 65. The accompanying table shows how the rising life expectancy has impacted the years spent in retirement thus accounting for a large portion of the financial paucity of the SS Trust Fund.

A 2020 analysis conducted by the Congressional Budget Office (CBO) found that increasing the full retirement age by two months per birth year until it reached age 70 for Americans born in 1978 or later would decrease total federal outlays by $72 billion for the period 2021-30. Thus, a female born in 1978 would have a full-retirement age of 68 years and 4 months in 2030. Using data from table 1 shows that this individual would spend an estimated 12.8 years in retirement, or almost the same as in 2000. Raising SS’s full retirement age makes sense because it corresponds with Americans’ lengthening lifespans and would lessen the burden on the future generations.

Ernie Goss

|

Instead of reducing monthly benefit payments, the retirement age could be changed with legislative action. The original Social Security Act of 1935 set the minimum age for receiving full retirement benefits at 65. The accompanying table shows how the rising life expectancy has impacted the years spent in retirement thus accounting for a large portion of the financial paucity of the SS Trust Fund.

A 2020 analysis conducted by the Congressional Budget Office (CBO) found that increasing the full retirement age by two months per birth year until it reached age 70 for Americans born in 1978 or later would decrease total federal outlays by $72 billion for the period 2021-30. Thus, a female born in 1978 would have a full-retirement age of 68 years and 4 months in 2030. Using data from table 1 shows that this individual would spend an estimated 12.8 years in retirement, or almost the same as in 2000. Raising SS’s full retirement age makes sense because it corresponds with Americans’ lengthening lifespans and would lessen the burden on the future generations.

Ernie Goss

Friday, December 16, 2022

U.S. Workers Losing Ground Since June 2020

Note that the hourly wage rate expanded slightly for the last three months of 2022. This is one factor pushing the Federal Reserve (FED) to raise interest rates. Powell, head of the Fed, is effectively saying to investors, "Read My Lips, We are going to continue to raise rates." Ernie Goss

Biden's Spending; Yellen's Price Fixing

Since taking office, the Biden Administration has passed a $1.9 trillion stimulus bill to fuel an economy that was already expanding at a very healthy pace. Now President Biden is advancing a so-called $2.0 trillion “infrastructure” bill.

To pay for a portion of this exploding spending, the president has called for an increase in the corporate income tax rate from 21% to 28%, and a boost in the income tax rate on households making more than $400,000. The added corporate tax rate is on top of state the assessment of 44 states and D.C. that have corporate income taxes on the books ranging from North Carolina’s single rate of 2.5% to a top marginal rate of 11.5% in New Jersey.

An increase in the federal corporate tax rate to 28 percent would raise the U.S. federal-state combined tax rate to an average of almost 34% and would be the highest among the 37 OECD nations which have an average corporate rate of 22% with lowest rates for Ireland at 12.5%, and Switzerland at 8.5%. This increase would harm U.S. economic competitiveness and increase the cost of U.S. firms. The Tax Foundation estimated that the hike would reduce long-run GDP growth by approximately one-fourth, eliminate 159,000 jobs, and reduce wages by 0.7%.

But instead of engaging in global competition, the Biden Administration is attempting to coerce OECD members into raising their rates. To quote ex-academic economist, Federal Reserve Chairman, and current U.S. Treasury Secretary Janet Yellen, “Destructive tax competition will only end when enough major economies stop undercutting one another and agree to a global minimum tax.”

I guess she only believed in market-based economics and competition when she was teaching macroeconomics at the University of California-Berkley. Welcome to the 21st Century Dr. Yellen. The U.S. must compete in the global economy, not attempt to fix prices, and limit competition. This is not legal for companies in the U.S., and should be verboten for OECD nations.

Sunday, September 18, 2022

Student Loan Forgiveness, Who Should Pay? An Alternative Solution

Suppose you go to the mall and purchase a widescreen monitor for a $1,000 paying for it with your newly minted Visa credit card. Unfortunately upon installation, you find it is defective and is not worth the fuel cost to return it to the merchant. Who pays the credit card balance? Will the U.S. taxpayer pick up the tab? NO! The cost will be borne by either the merchant, wholesaler, manufacturer, or you.

That is essentially what has happened to many college graduates who borrowed thousands to earn a college degree that, in many cases, entitled them to nothing more than a job selling jockey shorts at Montgomery Ward (I go back a long way).

Month-after-month, President Biden has delayed loan repayments for college tuition incurred at colleges ranging from the bottom to the top of the nation’s post-secondary institutions. Now he has proposed forgiving loans up to $20,000 for those making less than $125,000, and once again postponed payments for the rest. Estimates of the taxpayer cost of these actions have ranged from $300-$500 billion depending on the assumptions of the estimation model.

Why are the real beneficiaries, the colleges, sitting on the sidelines cheering on this costly proposal? A study by the New York Federal Reserve (https://tinyurl.com/4da9mc8b) concluded that 60 cents of every federal loan dollar simply landed in the coffers of colleges in the form of higher tuition revenue. As a result of this linkage, colleges have raised tuition five times the rate of inflation since 1980. At the same time college endowments soared to roughly $691 billion in 2022.

I propose that the cost of the student loan program be shared by the taxpayer, the university, and the student. The program will work very similar to unemployment pay systems in most states. Each semester, colleges will pay an experienced based fee that rises and falls with the past students’ repayment, or experience rating. Just as construction firms in Nebraska, due to higher historic layoff rates, pay more than four times the unemployment tax rate of non-construction firms, colleges with a history of student loan defaults and delinquencies will pay higher fees into the fund. This program will thus shift a portion of the cost of student loan defaults to those that helped create it---the colleges.

Transferring a portion of the cost of student loan defaults and delinquencies to the colleges will cause the institutions to 1) improve their educational processes to boost potential financial success in the labor market post-graduation, 2) improve the student selection process by including future economic viability of graduating students, 3) charge lower or higher tuition, depending on the salary outlook of particular majors, 4) insure that students receive true value or marketable skills from their studies. In the end, this program will slow the growth in tuition for all (even non-borrowers), and reduce taxpayer costs.

Ernie Goss

That is essentially what has happened to many college graduates who borrowed thousands to earn a college degree that, in many cases, entitled them to nothing more than a job selling jockey shorts at Montgomery Ward (I go back a long way).

Month-after-month, President Biden has delayed loan repayments for college tuition incurred at colleges ranging from the bottom to the top of the nation’s post-secondary institutions. Now he has proposed forgiving loans up to $20,000 for those making less than $125,000, and once again postponed payments for the rest. Estimates of the taxpayer cost of these actions have ranged from $300-$500 billion depending on the assumptions of the estimation model.

Why are the real beneficiaries, the colleges, sitting on the sidelines cheering on this costly proposal? A study by the New York Federal Reserve (https://tinyurl.com/4da9mc8b) concluded that 60 cents of every federal loan dollar simply landed in the coffers of colleges in the form of higher tuition revenue. As a result of this linkage, colleges have raised tuition five times the rate of inflation since 1980. At the same time college endowments soared to roughly $691 billion in 2022.

I propose that the cost of the student loan program be shared by the taxpayer, the university, and the student. The program will work very similar to unemployment pay systems in most states. Each semester, colleges will pay an experienced based fee that rises and falls with the past students’ repayment, or experience rating. Just as construction firms in Nebraska, due to higher historic layoff rates, pay more than four times the unemployment tax rate of non-construction firms, colleges with a history of student loan defaults and delinquencies will pay higher fees into the fund. This program will thus shift a portion of the cost of student loan defaults to those that helped create it---the colleges.

Transferring a portion of the cost of student loan defaults and delinquencies to the colleges will cause the institutions to 1) improve their educational processes to boost potential financial success in the labor market post-graduation, 2) improve the student selection process by including future economic viability of graduating students, 3) charge lower or higher tuition, depending on the salary outlook of particular majors, 4) insure that students receive true value or marketable skills from their studies. In the end, this program will slow the growth in tuition for all (even non-borrowers), and reduce taxpayer costs.

Ernie Goss

Wednesday, July 27, 2022

California Punishes High Income Earners: Iowa Leads, California Follows in Tax Competitiveness

In a 2022 ballot initiative, California progressives are pushing for passage of their deceptively entitled Clear Cars and Clear Air Act. In what represents a race to the bottom in economic performance, and in higher income taxes, the initiative raises the state’s top income tax rate by 1.75% to a non-competitive 15.1% surpassing New York City’s 14.8%. Despite a $100 billion 2022 state budget surplus, supporters of the $3.0 billion to $4.5 billion tax boost plan to use 80% of the booty to subsidize zero emission vehicles in the state.

Passage of the 2017 federal tax reform bill, which limited the deduction of state and local taxes on federal income returns to $10,000, made these California and New York taxes prohibitively high and incentivized the migration of individuals from high to low-income tax rate states. Furthermore, Covid-19 encouraged workers and entrepreneurs to work remotely and allowed them to exit cold, income tax hostile states for the warm environs of low-income tax rate states.

For example, the year after passage of the 2017 federal tax reform bill, real estate mogul, Barry Sternlicht, enhanced his net after tax income, and suntan, by moving operations of his Starwood Capital from high-tax Greenwich, Connecticut to no-tax Miami Beach, Florida. Likewise, Elon Musk, CEO of Tesla, moved company headquarters from high-tax California to no-tax Texas. Contrary to California, other states wasted no time in lowering income tax rates to hold on to workers, and/or encourage entrepreneurs to locate in their states. In the 2022 Iowa legislative session, Governor Kim Reynolds, and the Iowa Legislature, took the bold step of reducing the state’s income tax to a flat rate of 3.9%, thus joining 10 other states with some form of flat rate income tax.

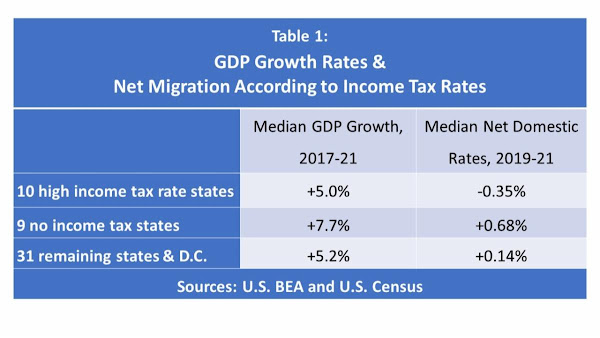

For 2021, the 10 highest income tax states, and their top rates were: *California 13.3%, Hawaii 11.0%, New Jersey 10.75%, Oregon 9.9%, Minnesota 9.85%, *District of Columbia 8.95%, New York 8.82%, Vermont 8.75%, Iowa 8.53% and Wisconsin 7.65%.

How did these states perform economically compared to all states, and to no-income tax states? Data since passage of the 2017 federal tax reform and 2021 support the wisdom of lowering, not raising the top income tax rate. GDP growth numbers and migration numbers are listed in Table 1. The data show a clear economic advantage for states with a lower top income tax rate.

Passage of the 2017 federal tax reform bill, which limited the deduction of state and local taxes on federal income returns to $10,000, made these California and New York taxes prohibitively high and incentivized the migration of individuals from high to low-income tax rate states. Furthermore, Covid-19 encouraged workers and entrepreneurs to work remotely and allowed them to exit cold, income tax hostile states for the warm environs of low-income tax rate states.

For example, the year after passage of the 2017 federal tax reform bill, real estate mogul, Barry Sternlicht, enhanced his net after tax income, and suntan, by moving operations of his Starwood Capital from high-tax Greenwich, Connecticut to no-tax Miami Beach, Florida. Likewise, Elon Musk, CEO of Tesla, moved company headquarters from high-tax California to no-tax Texas. Contrary to California, other states wasted no time in lowering income tax rates to hold on to workers, and/or encourage entrepreneurs to locate in their states. In the 2022 Iowa legislative session, Governor Kim Reynolds, and the Iowa Legislature, took the bold step of reducing the state’s income tax to a flat rate of 3.9%, thus joining 10 other states with some form of flat rate income tax.

For 2021, the 10 highest income tax states, and their top rates were: *California 13.3%, Hawaii 11.0%, New Jersey 10.75%, Oregon 9.9%, Minnesota 9.85%, *District of Columbia 8.95%, New York 8.82%, Vermont 8.75%, Iowa 8.53% and Wisconsin 7.65%.

How did these states perform economically compared to all states, and to no-income tax states? Data since passage of the 2017 federal tax reform and 2021 support the wisdom of lowering, not raising the top income tax rate. GDP growth numbers and migration numbers are listed in Table 1. The data show a clear economic advantage for states with a lower top income tax rate.

Friday, June 10, 2022

More Inflation, Less Consumer Confidence: Markets Take a Dive

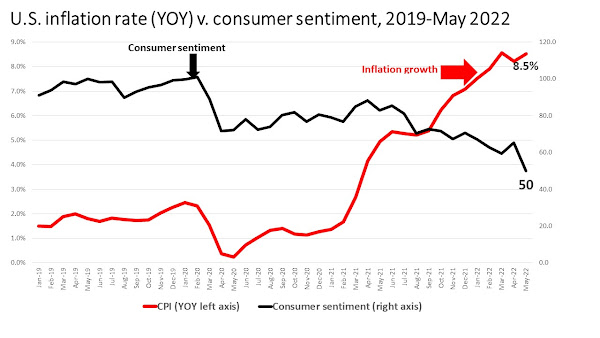

Today's releases of the May 2022 consumer price index and consumer sentiment were much worse than expected. I have graphed both measures below. This is the highest inflation recorded in 41 years, and the lowest consumer sentiment recorded since the index was launched in 1952.

The U.S. recession ended in the second quarter of 2020, yet the Biden Administration in 2021 pushed a $1.9 trillion stimulus spending program through Congress, and a $1.0 trillion infrastructure spending program.

To support this overspending, the Federal Reserve increased the U.S. money supply by 40% between 2020 and 2022. Note that the explosion in inflation and downturn in consumer sentiment preceded the Russian invasion of Ukraine.

The Federal Reserve is very apt to get more aggressive in raising short-term interest rates beginning next week. I expect the prime interest rate to rise from its current level of $4.0% to 6.0% by the first quarter of 2023. Ernie Goss

The Federal Reserve is very apt to get more aggressive in raising short-term interest rates beginning next week. I expect the prime interest rate to rise from its current level of $4.0% to 6.0% by the first quarter of 2023. Ernie Goss

The U.S. recession ended in the second quarter of 2020, yet the Biden Administration in 2021 pushed a $1.9 trillion stimulus spending program through Congress, and a $1.0 trillion infrastructure spending program.

To support this overspending, the Federal Reserve increased the U.S. money supply by 40% between 2020 and 2022. Note that the explosion in inflation and downturn in consumer sentiment preceded the Russian invasion of Ukraine.

Subscribe to:

Posts (Atom)